As the calendar year comes to a close, we wanted to take one final opportunity to examine the most recently released solar installation data from the New Jersey Office of Clean Energy. Throughout 2016 the New Jersey SREC market has been profoundly influenced by the implications of the data in these reports. After experiencing the type of price volatility we’ve seen in 2016, our hope is that market participants will welcome some added insight into these numbers and will consider this analysis as they begin to make projections for 2017.

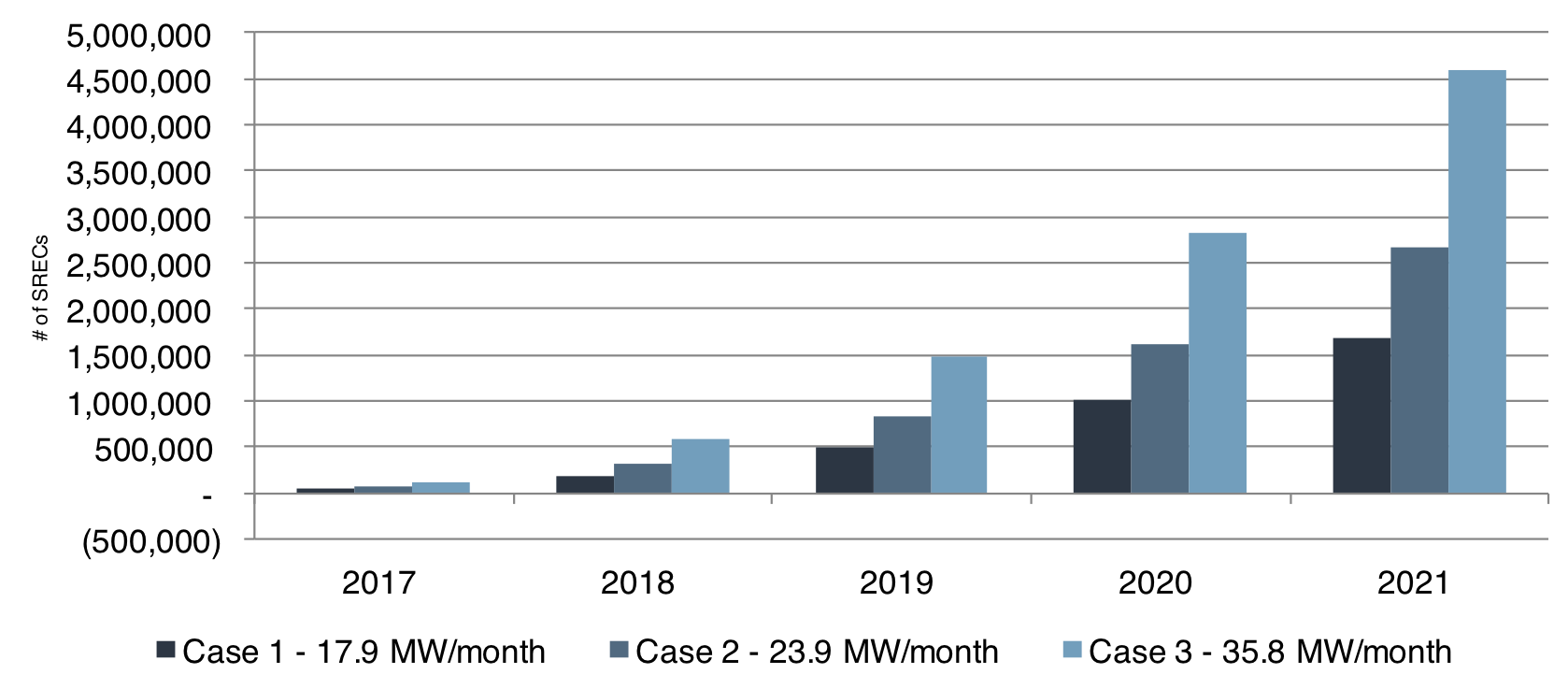

You can find our most recent capacity presentation here.

As of 11/30/2106, the latest NJOCE Solar Installation Report showed an increase of 26.7MW of installed capacity since it was last issued as of 10/30/16. Almost 20MW of that increase came from reported installations in October and November, with the balance distributed relatively evenly back to June 2015.

- 10.3MW added in November 2016

- 9.6MW added in October 2016

- 4.6MW added July through September 2016

- 2.2MW added June 2015 through June 2016

**Regular readers of these reports will also notice that a significant amount of capacity was “added” to the period from 2001 to May 2015, although this was simply a reclassification of previously reported capacity in order to improve the accuracy of the information presented. **

Within this report, a trend which we had previously noted has become more clearly defined. Assuming that the November figure for installed capacity will be revised upward in future reports to a degree similar to the prompt months in prior data releases, we see that the average monthly rate has fallen drastically from the first half of the year to the second. Through the first six months of 2016, the New Jersey solar market was adding just over 33MW/month. Assuming the reported November installation number doubles due to future upward revisions, since July that monthly average has now dropped to 20MW/month. That represents a 40% drop in new installations.

Although there were undoubtedly a range of factors that contributed to this sudden shift, lower SREC pricing almost certainly played a central role in this change of trend. When extrapolated out into the future, the extremely aggressive build rates observed in Q1 and Q2 of 2016 indicated a market that would very quickly become oversupplied as the pace of development overtook the rate of RPS growth. This expectation of future imbalance led to a precipitous decline in prices, bringing the NJ SREC spot market down from highs in the $290s to lows in the $200s. This decline meant developers experienced further difficulty finding adequate funding to support their pipeline of projects. The consequence has been that many projects that don’t qualify for residential rates of electricity – those projects who would otherwise depend on healthy SREC prices to be economically feasible – simply didn’t get built. This is clearly apparent when comparing the three month periods ending in July 2016 and November 2016:

A closer examination of the data reveals another powerful shift in industry trends. Commercial and residential build rates have historically kept a somewhat even balance with respect to one another. In 2015, commercial and residential capacity made up 41% and 52%, respectively, of total installations in that year. In the first half of 2016, that balance was 58% and 40%, respectively. Since July 2016, that balance has now shifted to 23% and 64%. While the residential market has remained strong, the larger commercial-sized systems have experienced very real difficulty. Again, this shift is not solely due to SREC pricing, but the significant decline in the amount of funding available from the SREC markets undoubtedly played a powerful role.

As always, we want to apply this information to create better informed opinions regarding the future of the market. The recent slowdown in new installation has further supported the idea that EY2017 will remain fairly balanced in terms of supply and demand. Across a range of scenarios, 2017 will most likely remain well balanced with a projected oversupply of only 9-11%. Barring a drastic acceleration in new installations, 2018 is also projected to remain fairly balanced. 2019 and beyond, however, take on a much different dynamic.

Even under modest growth scenarios, the current RPS can again be overwhelmed by the growth of the New Jersey solar market in a matter of years. It is important to note that the pricing of all financial products – SRECs included – is determined by a combination of current market conditions as well as expectations of market conditions in the future. Even though 2017 and 2018 appear to be years of relative balance, a drastic oversupply in the later years of the New Jersey market could easily have an adverse affect on pricing in the near term. Without some type of legislative amendment to the current state RPS schedule, the New Jersey SREC market could feasibly experience a prolonged period of depressed pricing which would signal a new, harsher economic reality for solar market participants across all segments of solar installation.

It is SRECTrade’s opinion that the market would be best served by proactively supporting any available means of expanding the state’s RPS schedule to account for this future growth. In order to successfully support the solar market, any such solution will need to focus on the longer term expansion of the SREC program. There have been several different proposals debated amongst industry participants, all of which have their own merits, but the fact remains that ANY expansion is better than none at all. If the industry chooses not to take this opportunity to expand the RPS program, developers will face an increasing probability of further market contraction and slower growth.

We will continue to update you with any new data as it becomes available. Please feel free to reach out to your SRECTrade brokerage coverage with any questions or comments you may have, we are always willing and eager to discuss our analysis with all members of the market.

We wish continued success and happiness to all of our friends and partners in the renewable energy industry, and we look forward to working together again in 2017!

**This report was updated on 4/20/2017 to address an error in the oversupply projection model which resulted in the oversupply being slightly understated. This has now been corrected**

Disclaimer. This document, data, and/or any of its components (collectively, the “Materials”) are for informational purposes only. The Materials are not intended as investment, tax, legal, or financial advice, or as an offer or solicitation for the purpose or sale of any financial instrument. SRECTrade, Inc. does not warranty or guarantee the market data or other information included herein, as to its completeness, accuracy, or fitness for a particular purpose, express or implied, and such market data and information are subject to change without notice. Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance. Any comments or statements made herein do not necessarily reflect those of SRECTrade, Inc. SRECTrade, Inc. may have issued, and may in the future issue, other communications, data, or reports that are inconsistent with, and reach different conclusions from, the information presented herein.

Copyright. This document is protected by copyright laws and contains material proprietary to SRECTrade, Inc. This document, data, and/or any of its components (collectively, the “Materials”) may not be reproduced, republished, distributed, transmitted, displayed, broadcasted or otherwise disseminated or exploited in any manner without the express prior written permission of SRECTrade, Inc. The receipt or possession of the Materials does not convey any rights to reproduce, disclose, or distribute its contents, or to manufacture, use, or sell anything that it may describe, in whole or in part. If consent to use the Materials is granted, reference and sourcing must be attributed to the Materials and to SRECTrade, Inc. If you have questions about the use or reproduction of the Materials, please contact SRECTrade, Inc.