With the close of the Maryland 2017 compliance year approaching, we thought it would be relevant to provide an update on where the current market stands, including recent happenings that could impact the future Renewable Portfolio Standard (RPS) requirements. Click here for our full presentation.

This year started off slightly more positive as the market moved up off its early Q4 2017 lows of about $5.00-6.00/SREC. Recent spot transactions have been ranging between $7.00-7.50/SREC. Additionally, the MD2018 and MD2019 forward markets have trended up into the $8.50-$10.50/SREC range depending on vintage and transaction size. It is likely that a combination of the 2017 compliance year coming to a close as well as standard offer service electricity load auctions taking place in late January had a positive price impact through increasing buy side demand.

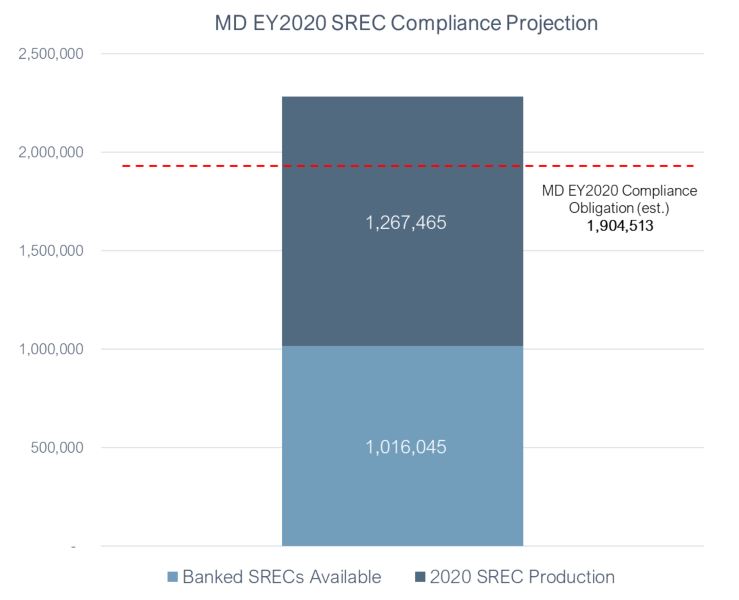

Under the current RPS requirements, the MD SREC market is fundamentally oversupplied. Solar build rates remained strong through the end of 2017 and the 100 megawatt (MW) Great Bay project is now registered in PJM GATS. Excluding the Great Bay project, however, the market experienced a 15.7% decline in average MW build per month in the last 6 months versus the last 12 months (through November). Even though the rates per month are declining, the market saw a push of project registrations heading in to the close of 2017, which is typically normal at year end (i.e. excluding Great Bay, 33.9 MW were registered in GATS through November 2017 vs. 26.7 MW through August 2017).

The most meaningful news for the Maryland RPS is the introduction of Senate Bill 732. The bill aims to increase the overall RPS requirements to 50% by 2030 and increase the solar carve out requirements to 14.5% by 2028, with a large step up to 5.5% in 2019. In addition to increasing the MD RPS, the bill also reduces the Alternative Compliance Payment (ACP) for both the Tier I and solar carve out requirements. Summary charts below outline the proposed changes to the solar carve out portion of the RPS, including both RPS % increases and ACP decreases.

The bill had its first reading in the Senate Finance Committee in early February. It is scheduled to be heard in the house (HB1453) on March 5th and then in the Senate on March 6th. As demonstrated in the Maryland SREC Update presentation above, the increase in the RPS % under SB732 would allow for Maryland’s solar market to continue to build at rates in excess of current last 12 month averages (i.e. 20.3 MW/month). This would allow the market to develop a variety of project types including larger, utility scale projects that the state has seen over the past few years. While the step up to a 5.5% solar requirement in 2019 is substantial, our presentation does not take into consideration the impact of exempt electric load that would only be eligible under the old RPS schedule given already signed electricity supply agreements. Exempt load would reduce estimated demand in the earlier years of the RPS increase under SB732, but nonetheless the RPS increase would have a substantial effect on increasing the demand for SRECs and solar supply in the state of Maryland.

SRECTrade will continue to track the status of this legislation. In the meantime, please feel free to contact us with any questions.