SRECTrade SREC Markets Report: August 2012

The following post outlines the megawatts of solar capacity certified and/or registered to create SRECs in the Solar REC markets SRECTrade currently serves.

A PDF copy of this table can be found here.

")

PJM Eligible Systems

As of this writing, there were 28,155 solar PV and 437 solar thermal systems registered and eligible to create SRECs in the PJM Generation Attribute Tracking System (GATS). Of these eligible systems, 185 (0.65%) have a nameplate capacity of 1 megawatt or greater, of which 18 systems are greater than 5 MW. The largest system, the PSE&G utility pole mount project located in New Jersey, is 25.1 MW, and the second largest, located in Maryland is 16.1 MW. The third largest system, at 12.5 MW, is located in New Jersey.

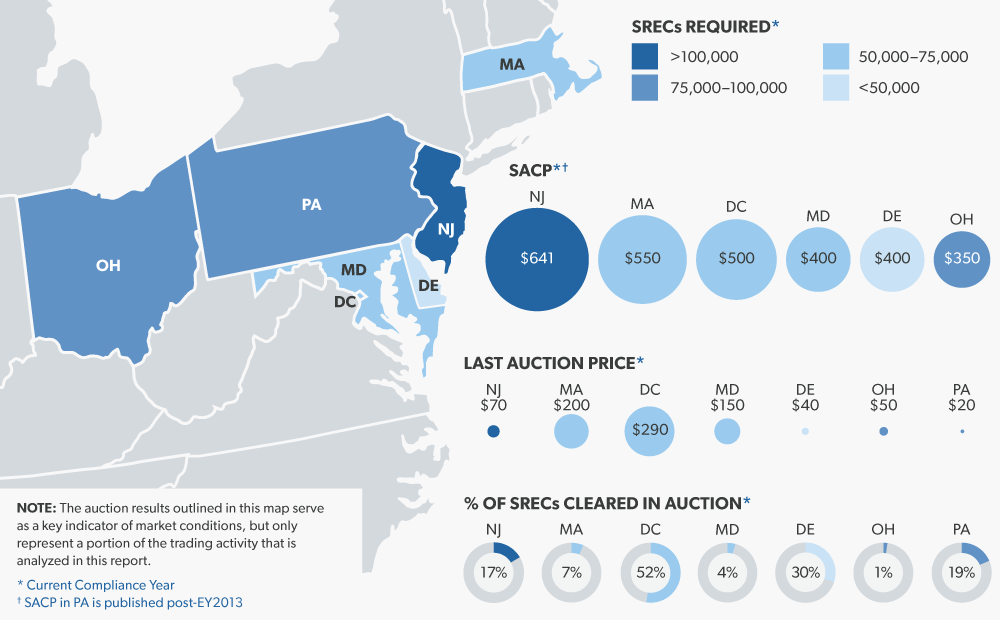

Delaware: The reporting year 2012 (6/1/12 – 5/31/13) requirement for DE equates to approximately 48,100 SRECs being retired. If all retired SRECs were of DE2012 vintage, approximately 40.1 MW would need to be operational all year long. As of September 11, 2012, 28.8 MW of solar capacity was registered and eligible to create DE SRECs in PJM GATS. As of September 11, 2012, PJM GATS reported the issuance of approximately 5,900 DE2012. Additional SRECs from prior eligible periods may also impact the market should there be a demand for these older vintage SRECs.

Maryland: As of September 11, 2012, 72.5 MW of MD sited solar capacity was registered to create MD eligible SRECs. A large increase came from a 16.1 MW project Constellation Energy commissioned at Mount St. Mary’s University. The 2012 reporting year requirement for MD equates to approximately 67,310 SRECs being retired. If all retired SRECs were of MD2012 vintage, approximately 56.1 MW would need to be operational all year long. As of September 11, 2012, PJM GATS reported the issuance of approximately 41,800 MD2012 SRECs. Lastly, there are MD sited SRECs available from prior eligible periods, which could be utilized for compliance needs in 2012.

New Jersey: The New Jersey 2012 and 2013 reporting years require 442,000 and 596,000 eligible SRECs, respectively. For 2012, this equates to approximately 368 MW of capacity being operational all year long and 496.7 MW for 2013, assuming all requirements were met with current vintage year SRECs. As of September 11, 2012, 843.3 MW of solar capacity was registered and eligible to create NJ SRECs in PJM GATS. While this figure represents all projects registered in GATS, there are recently installed projects awaiting issuance of a New Jersey state certification number. This delay results in a portion of installed projects not yet represented in the 843.3 MW figure. As of July 31, 2012 the NJ Office of Clean Energy (NJ OCE) reported that 852.7 MW of solar had been installed in NJ. Estimates for August 2012 show a total of 876.0 MW. On July 23, NJ Governor, Chris Christie, signed into law legislation to increase the Solar RPS requirements. For details see the following: NJ Governor Christie Signs Bill to Increase Solar Requirements. As of September 11, 2012, PJM GATS reported the issuance of approximately 699,200 NJ2012 SRECs. This figure surpasses the current 2012 compliance year requirement of 442,000 SRECs by approximately 257,200 SRECs. Additionally, the second month of RY2013 generation was issued at the end of August. GATS reported a total of 196,700 total NJ2013 SRECs for the compliance year to date were issued; approximately 33% of the current year’s obligation (not considering the eligible oversupply from NJ2012).

Ohio: Ohio’s 2012 RPS solar target requires approximately 95,300 SRECs to be retired by the end of the compliance period. At least 50% of the SREC requirement must come from systems sited in the state. As of September 11, 2012, 50.2 MW of in-state capacity and 96.7 MW of out-of-state capacity were eligible to generate OH SRECs. As of September 11, 2012, GATS issued approximately 40,400 in-state and 71,900 out-of-state OH2012 eligible SRECs. Additional SRECs from prior years are also eligible for the current compliance period, which may impact the current year’s requirements.

Pennsylvania: The reporting year 2012 and 2013 requirements for PA equates to retiring approximately 49,450 and 78,750 eligible SRECs, respectively. If all compliance obligations were met using 2012 and 2013 vintage SRECs, approximately 41.2 and 65.6 MW would need to be operational all year long within each compliance period. As of September 11, 2012, 222.4 MW of solar capacity was registered and eligible to create PA compliant SRECs. As of September 11, 2012, PJM GATS reported the issuance of approximately 220,000 PA2012 SRECs. Given the oversupply during previous reporting years, there are also SRECs from the 2010 and 2011 reporting years eligible for the PA2012 compliance period. Additionally, as of September 11, 2012 GATS reported approximately 52,000 PA2013 SRECs were issued.

Washington, DC: DC’s 2012 RPS amended solar target requires approximately 61,180 SRECs to be retired by the end of the compliance period. The figures displayed above demonstrate the capacity of systems eligible to create DC SRECs moving forward. These SREC and capacity figures do not take into consideration the amount of electricity delivered into the district that may be exempt from complying with the Distributed Generation Amendment Act increases, considering some electricity contracts may have been signed prior to the amendment’s implementation. As of September 11, 2012, 24.4 MW of capacity was eligible to generate DC SRECs. Additionally, as of September 11, 2012, GATS reported the issuance of approximately 18,000 DC2012 eligible SRECs. SRECs from prior years are also eligible for the current compliance period, which may impact the current year’s requirements.

Massachusetts DOER Qualified Projects

As of September 11, 2012, there were 3,134 MA DOER qualified solar projects; 3,118 operational and 16 not operational. Total qualified capacity is 121.3 MW, 110.4 of which is operational and 10.9 MW not operational. Electricity suppliers providing power to the state need to acquire approximately 73,400 SRECs in 2012. According to NEPOOL GIS, 14,479 Q1 2012 SRECs were issued on July 15, 2012. Additionally, 53,359 MWhs were reported to the MassCEC production tracking system for the 5 months covering April-August 2012.

Capacity Summary By State

The tables above demonstrate the capacity breakout by state. Note, that for all PJM GATS registered projects, each state includes all projects certified to sell into that state. State RPS programs that allow for systems sited in other states to participate have been broken up by systems sited in-state and out-of-state. Additional detail has been provided to demonstrate the total capacity of systems only certified for one specific state market versus being certified for multiple state markets. For example, PA includes projects only certified to sell into the PA SREC market, broken out by in-state and out-of-state systems, as well as projects that are also certified to sell into PA and Other State markets broken out by in state and out of state systems (i.e. OH, DC, MD, DE, NJ). PA Out of State includes systems sited in states with their own state SREC market (i.e. DE) as well as systems sited in states that have no SREC market (i.e. VA). Also, it is important to note that the Current Capacity represents the total megawatts eligible to produce and sell SRECs as of the noted date, while the Estimated Required Capacity – Current and Next Reporting Year represents the estimated number of MW that need to be online on average throughout the reporting period to meet the RPS requirement within each state with only that particular compliance period vintage. For example, New Jersey needs approximately 368 MW online for the entire 2012 reporting year to meet the RPS requirement with 2012 vintage SRECs only. SRECs still available from prior eligible periods can also impact the Solar RPS requirements. Additionally, the data presented above does not include projects that are in the pipeline or currently going through the registration process in each state program. This data represents specifically the projects that have been approved for the corresponding state SREC markets as of the dates noted.

Note: SREC requirements for markets without fixed SREC targets have been forecast based based on EIA Report updated 11/15/11 “By End-Use Sector, by State, by Provider”. Projected SRECs required utilizes the most recent EIA electricity data applying an average 1.5% growth rate per forecast year. The state’s RPS Solar requirement is then multiplied by forecast total electricity sales to arrive at projected SRECs required. Projected capacity required is based on a factor of 1,200 MWh in PJM states and 1,130 MWh in MA, generated per MW of installed capacity per year.

")