Last week, members of the SRECTrade team attended MDV-SEIA’s Solar Focus Conference in Washington, D.C. The conference’s focus was on “cracking the code for East Coast solar”, and the subject matter covered a wide variety of issues relevant to the solar industry across the Mid-Atlantic region. In particular, the conference provided a forum for in-depth conversations around the future of critical, although challenged, state markets such as Pennsylvania and Maryland.

SRECTrade’s Director of Environmental Markets, Brett Waikart and our Director of Regulatory Affairs and General Counsel, Allyson Browne were invited to speak about the Maryland and Pennsylvania markets, respectively. Brett’s presentation covered the fundamentals of the Maryland SREC market and laid out hypothetical future scenarios assuming various RPS carve-out schedules and build rates. Allyson’s presentation focused on the composition of Pennsylvania’s electricity market and emphasized different aspects of the state’s Alternative Energy Portfolio Standard (AEPS) structure that could be adjusted in order to improve market conditions. Their presentations are included below, along with a brief synopsis of the analysis provided.

Maryland SREC Update – November 2016

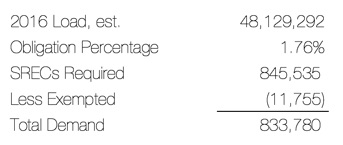

Little has changed in the overall degree of oversupply in the Maryland spot market since our last post in September. There have been no changes to official RPS policy, and supply continues to far outstrip the demand levels set by the RPS compliance schedule. As can be seen in the snapshot below, as of November 15th there were approximately 156k CY14 and CY15 SRECs still available for sale and another 477k CY16 SRECs that had been generated in the current year. Assuming that recent build rates continue through the end of 2016, we anticipate another 89k SRECs to be generated before the year is over. When compared to the MD16 RPS obligation of approximately 431k SRECs, these numbers indicate that we are oversupplied by a little more than 291k SRECs, or 68% of the current RPS demand requirement.

While this degree of oversupply is substantial, the monthly build rate numbers confirm that weaker project economics, caused by depressed SREC prices, have indeed slowed the installation of new capacity significantly. The average amount of new capacity added over the last three months has slowed to just less than 10MW/month, as compared to just less than 30MW/month in the first quarter of 2016. Also notable is that we have not seen the installation of a single asset greater than 1MW in capacity reports since June. You can clearly see the trend lower in the graph below, which illustrates the quarterly sum of new capacity brought online over the last year.

With the MD SREC market now fully reflecting the current degree of oversupply, and the effects now being felt by the asset development industry, stakeholders can agree that the time has come to find a solution. The Maryland market has now fully outgrown the trajectory previously laid out for it through the current RPS schedule. With that in mind, we now present a third scenario in our MD Capacity Presentation. In addition to our typical supply and demand projections under the current RPS and the RPS proposed through HB1106, we now include an analysis illustrating the potential market conditions that would result from a more aggressive RPS schedule. You will find our results in the slide deck provided below.

Our full capacity presentation can be found here.

Pennsylvania Policy Update

The concept of oversupply is even more familiar to Pennsylvania’s SREC market. Although the state’s AEPS targets exceed those of other PJM state RPS targets on an absolute basis, the state has been fundamentally oversupplied for years due to the design of its program.

In her presentation, Allyson takes a holistic look at Pennsylvania’s electricity market and generation mix and applies this foundation to the state’s AEPS design. The result is a structural oversupply that will require several supply- and demand-side adjustments before the market will be able to rebound and achieve supply-demand balance.

After providing this framework for the panel’s discussion, Allyson addresses Pennsylvania’s work towards compliance with the EPA’s Clean Power Plan (despite its now uncertain future) and identifies possible routes for reinvigorating Pennsylvania’s solar market.

Allyson’s full presentation can be viewed here.

As always, please feel free to reach out to your coverage on the SRECTrade brokerage desk to discuss any observations or comments you may have regarding our analysis or your view of the SREC markets. We will continue to update our analysis and provide you with any new information we receive as it becomes relevant.

Disclaimer. This document, data, and/or any of its components (collectively, the “Materials”) are for informational purposes only. The Materials are not intended as investment, tax, legal, or financial advice, or as an offer or solicitation for the purpose or sale of any financial instrument. SRECTrade, Inc. does not warranty or guarantee the market data or other information included herein, as to its completeness, accuracy, or fitness for a particular purpose, express or implied, and such market data and information are subject to change without notice. Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance. Any comments or statements made herein do not necessarily reflect those of SRECTrade, Inc. SRECTrade, Inc. may have issued, and may in the future issue, other communications, data, or reports that are inconsistent with, and reach different conclusions from, the information presented herein.

Copyright. This document is protected by copyright laws and contains material proprietary to SRECTrade, Inc. This document, data, and/or any of its components (collectively, the “Materials”) may not be reproduced, republished, distributed, transmitted, displayed, broadcasted or otherwise disseminated or exploited in any manner without the express prior written permission of SRECTrade, Inc. The receipt or possession of the Materials does not convey any rights to reproduce, disclose, or distribute its contents, or to manufacture, use, or sell anything that it may describe, in whole or in part. If consent to use the Materials is granted, reference and sourcing must be attributed to the Materials and to SRECTrade, Inc. If you have questions about the use or reproduction of the Materials, please contact SRECTrade, Inc.

Tweet