Last Friday, SRECs generated in Q3 of 2015 were issued to all qualified asset owners in the Massachusetts SREC-I and SREC-II programs. The additional liquidity brought to the market helped refocus attention on the MA SREC program after the beginning of the year was dominated by action in the New Jersey market. Given the renewed attention to the Massachusetts markets we have adjusted our capacity models to reflect the most current supply and demand figures.

Our most recent MA SREC-II capacity presentation can be found here.

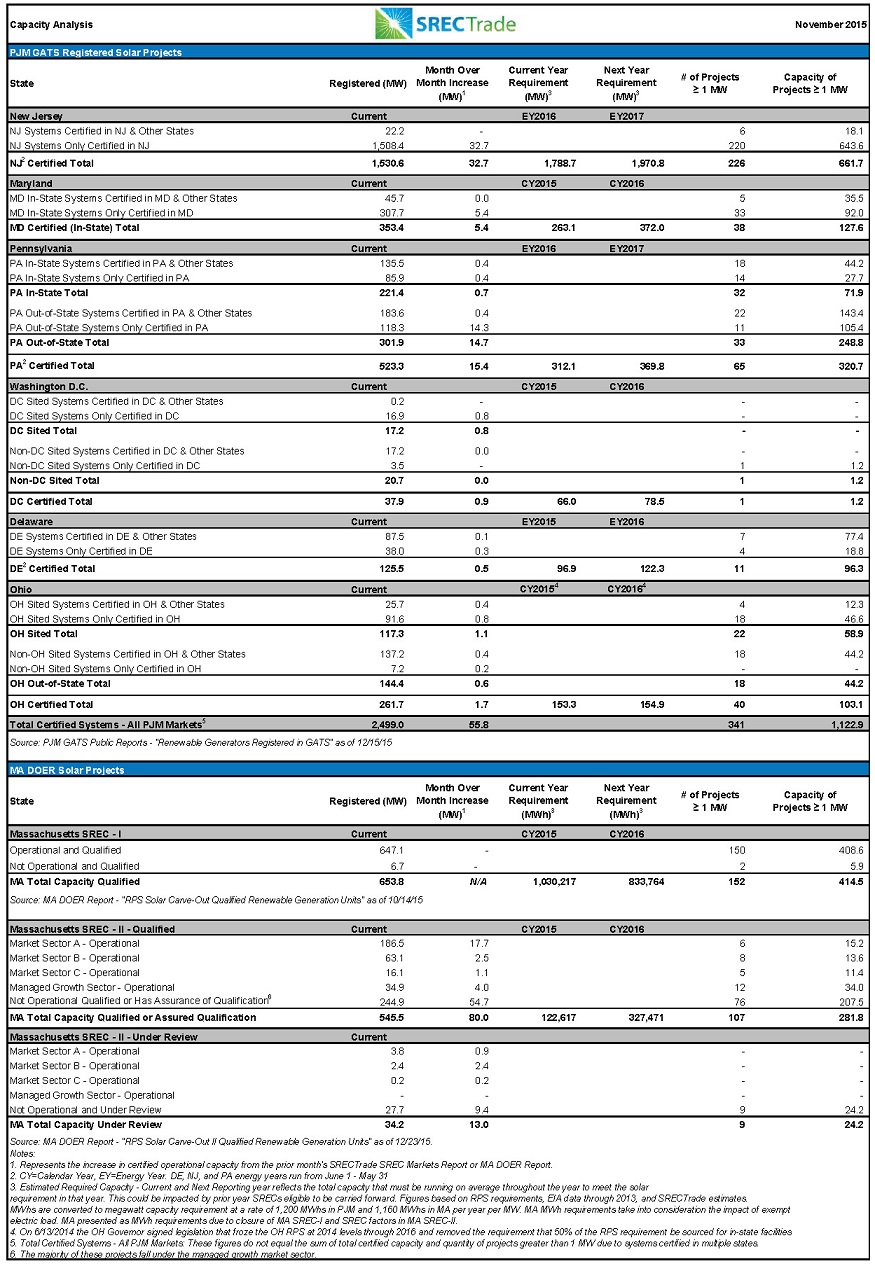

As compared to our last MA Capacity Update, the Trailing Six Month (TSM) average build rate is only marginally higher at 18.7 MW/mo as compared to the Trailing Twelve Month (TTM) 17.8 MW/mo. The greatest contrast is between the three months ending in September 2015 and December 2015, with asset developers installing twice as much SREC-II eligible capacity over the summer as what was installed in the fall.

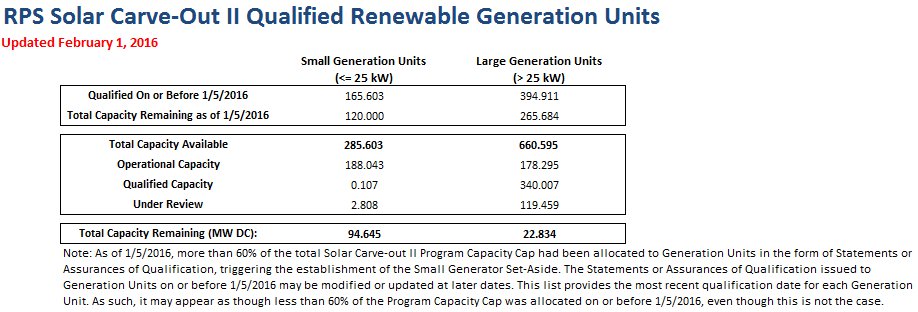

Using these updated numbers we can begin to predict the degree of over or under supply in the upcoming year. Due to the methodology employed by the MA DOER we already know what the 2016 compliance requirement will be. We can also use the most recent year to date build (YTD) rate, 17.9 MW/month, as our base-case assumption for future 2016 build. What is important to add to this analysis, however, is the 120 MW carve out that the MA DOER announced in their most recent bulletin. Of the total 946.2 MW of SREC-II eligible capacity (1,600 MW of total covered capacity less the 658.3MW covered by SREC-I) we know that 575.1 MW have already been qualified for SREC-II. This leaves 371.1MW still available for new construction, however we now know that since we have passed the 60% threshold of total SREC eligible capacity, 120MW of that remainder will be reserved for projects less than 25KW. This leaves just 251.1MW for larger scale projects under the current program.

Holding our most recent YTD build rate (17.9 MW/mo) constant and using the previously set 2016 compliance obligation, we see the MA SREC-II market finishing 2015 oversupplied by 78,957 SRECs and 2016 oversupplied by 226,537. These figures are equivalent to 64.4% and 69.2% oversupplied, respectively. Slide 8 of our MA SREC-II presentation also illustrates potential upper and lower bounds for 2016 build rates, set at 75% and 150% of 2015 YTD average monthly build. Across all scenarios we project that the market will finish 2016 oversupplied, somewhere between a range of 56.7% to 81.7%

As always, this analysis is informational only in purpose in order to help explain the implications of recently reported MA SREC-II eligible build rates. We will continue to watch the markets closely and stay on top of new MA capacity data as it is updated by the Massachusetts DOER.

Disclaimer. This document, data, and/or any of its components (collectively, the “Materials”) are for informational purposes only. The Materials are not intended as investment, tax, legal, or financial advice, or as an offer or solicitation for the purpose or sale of any financial instrument. SRECTrade, Inc. does not warranty or guarantee the market data or other information included herein, as to its completeness, accuracy, or fitness for a particular purpose, express or implied, and such market data and information are subject to change without notice. Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance. Any comments or statements made herein do not necessarily reflect those of SRECTrade, Inc. SRECTrade, Inc. may have issued, and may in the future issue, other communications, data, or reports that are inconsistent with, and reach different conclusions from, the information presented herein.

Copyright. This document is protected by copyright laws and contains material proprietary toSRECTrade, Inc. This document, data, and/or any of its components (collectively, the “Materials”) may not be reproduced, republished, distributed, transmitted, displayed, broadcasted or otherwise disseminated or exploited in any manner without the express prior written permission ofSRECTrade, Inc. The receipt or possession of the Materials does not convey any rights to reproduce, disclose, or distribute its contents, or to manufacture, use, or sell anything that it may describe, in whole or in part. If consent to use the Materials is granted, reference and sourcing must be attributed to the Materials and to SRECTrade, Inc. If you have questions about the use or reproduction of the Materials, please contact SRECTrade, Inc.