The Department of Energy Resources (DOER) published an updated list of projects with a Statement of Qualification (SQA) on August 25, 2016. Since the last update in July not much has changed in the SREC-II landscape. Expected oversupply still remains the reality reflected in pricing for 2016. Similarly, monthly build-rates are more or less unchanged. The total installed capacity increased 65MW since the last update, bringing us to 573.54 MW. You can find our in-depth analysis here. Below, please find some highlights.

Based on the latest data, there are currently 573.54 MW of operational assets, with an additional 956.87 MW that is qualified, but not operational:

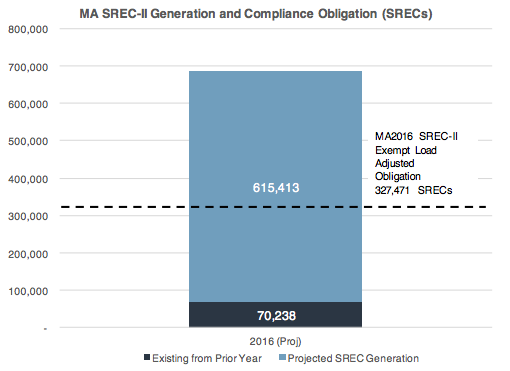

Finally, based on current build rates, we continue to see a gross oversupply for the MA2016 SREC-II market:

Thus far, the market has generated 82,758 MA2016 SREC-IIs and based on current build-rates and installed capacity, we estimate an additional 473,084 SRECs coming later in the year. Adding in the re-minted volumes of 67,046, we see a potential pool of supply upwards of 622,888. Compare that supply figure to the demand side of approximately 327,471 and we conclude the market is oversupplied by 90%. In other words, nearly half of all MA2016 SRECs may find their way to the Solar Credit Clearinghouse Auction next year.

Disclaimer. This document, data, and/or any of its components (collectively, the “Materials”) are for informational purposes only. The Materials are not intended as investment, tax, legal, or financial advice, or as an offer or solicitation for the purpose or sale of any financial instrument. SRECTrade, Inc. does not warranty or guarantee the market data or other information included herein, as to its completeness, accuracy, or fitness for a particular purpose, express or implied, and such market data and information are subject to change without notice. Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance. Any comments or statements made herein do not necessarily reflect those of SRECTrade, Inc. SRECTrade, Inc. may have issued, and may in the future issue, other communications, data, or reports that are inconsistent with, and reach different conclusions from, the information presented herein.

Copyright. This document is protected by copyright laws and contains material proprietary to SRECTrade, Inc. This document, data, and/or any of its components (collectively, the “Materials”) may not be reproduced, republished, distributed, transmitted, displayed, broadcasted or otherwise disseminated or exploited in any manner without the express prior written permission of SRECTrade, Inc. The receipt or possession of the Materials does not convey any rights to reproduce, disclose, or distribute its contents, or to manufacture, use, or sell anything that it may describe, in whole or in part. If consent to use the Materials is granted, reference and sourcing must be attributed to the Materials and to SRECTrade, Inc. If you have questions about the use or reproduction of the Materials, please contact SRECTrade, Inc.

Tweet