The California Air Resources Board (CARB) published quarterly program data for the Low Carbon Fuel Standard (LCFS) on June 30, 2023 and announced another workshop for August 16 to discuss changes to the program.

Credit Bank Adds 1.3M Net Credits After Sluggish Q1

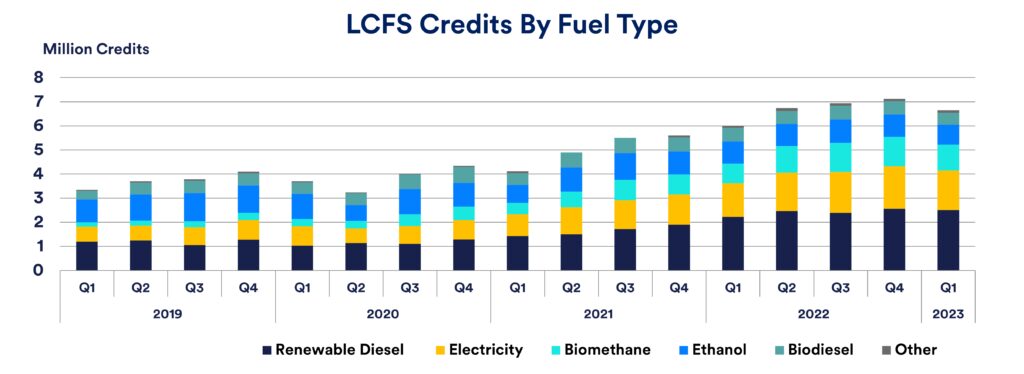

The cumulative credit bank, a measure of net credit generation over the lifetime of the program, grew for an eighth consecutive quarter and now stands at 16.5M credits. Deficits were down in Q1 (-3%), driven largely by a decline in gasoline volume (-9%). Credits from all sources (-6%) fell for the first time in 2 years driven in part by reductions in volume from electricity (-5%), biodiesel (-3%), and ethanol (-2%). Average carbon intensities (CI) were up across the major credit sources as well, including RNG (+21%), biodiesel (+8%), RD (+9%), and electricity (+3%). Finally, the more stringent CI targets for 2023 kicked in, which reduces the number of credits per unit of low carbon fuel when compared to 2022.

EV Credits Take a Step Back in Q1

Credits from electricity fell last quarter (-7%) for the first time since the COVID pandemic, driven primarily by a 12% decline in residential EV charging credits which are issued to utilities based on a formula. Credits also decreased across other categories including eForklifts (-1%), ocean-going vessels (-13%) and fixed-guideways (-11%). EVs still remain the second largest source of credits under the LCFS and among the fastest growing fuel type.

What’s Next for CA LCFS?

CARB scheduled a workshop on August 16 to present updates to their model that is used to assess the feasibility and economic impact of proposed changes to the program, including establishing more stringent 2030 CI targets. In the previous workshop held in May, CARB staff had reiterated their intent to initiate a formal rulemaking process to make changes to the LCFS by this summer, with a targeted implementation date of January 1, 2024.

CARB will release Q2 2023 program data by October 31, 2023.

Tweet