225 CMR 14.00 Renewable Portfolio Standard Class I Regulations

On January 3, 2014, the Massachusetts Department of Energy Resources (DOER) filed revisions to the 225 CMR 14.00 Renewable Portfolio Standard Class I regulation. The email announcement is available here. The redlined, unofficial version of this draft is available on the DOER website, and the official version of the draft regulation will be published in the Massachusetts Register on January 17, 2014. This filing begins the formal rulemaking process.

The primary objectives of the revisions are twofold: 1) to establish the second phase of the Solar Carve-Out program (the SREC-II program); and 2) to revise the RPS Class I program to address previously identified needs to improve the program design. Next stages for the rulemaking process and a few excerpts of the draft are detailed below.

I. Continuation of Rulemaking Process

A. Public Hearing

The DOER will hold a public hearing on January 24, 2014 from 1:00 to 3:00 pm to receive oral and written comments on the proposed regulations. The hearing will be held at the Gardner Auditorium of the Massachusetts State House in Boston, MA. Parties interested in presenting oral testimony at the hearing are requested to provide written copies of their testimony.

B. Written Comments

Per the DOER: Written comments will be accepted beginning on January 3, 2014 and ending at 5:00 pm on January 29, 2014. Please submit written comments electronically to DOER.SREC@state.ma.us or to Michael Judge, via mail to the Department of Energy Resources, 100 Cambridge Street, Suite 1020, Boston, MA 02114.

II. Selected Excerpts

A. Eligibility for SREC-II

Section 14.05(9)(b) specifies that a Solar Carve-Out II (SREC-II) Renewable Generation Unit must have a Commercial Operation Date on or after January 1, 2012 and must not be qualified as a Solar Carve-Out Renewable Generation Unit (that is, qualified under the SREC-I program). Section 14.06(4)(c) states that the RPS Effective Date for SREC-II facilities shall be the Commercial Operation Date or the first day following the calendar quarter in which the Unit receives its Statement of Qualification (see Part C. below), whichever is earlier.

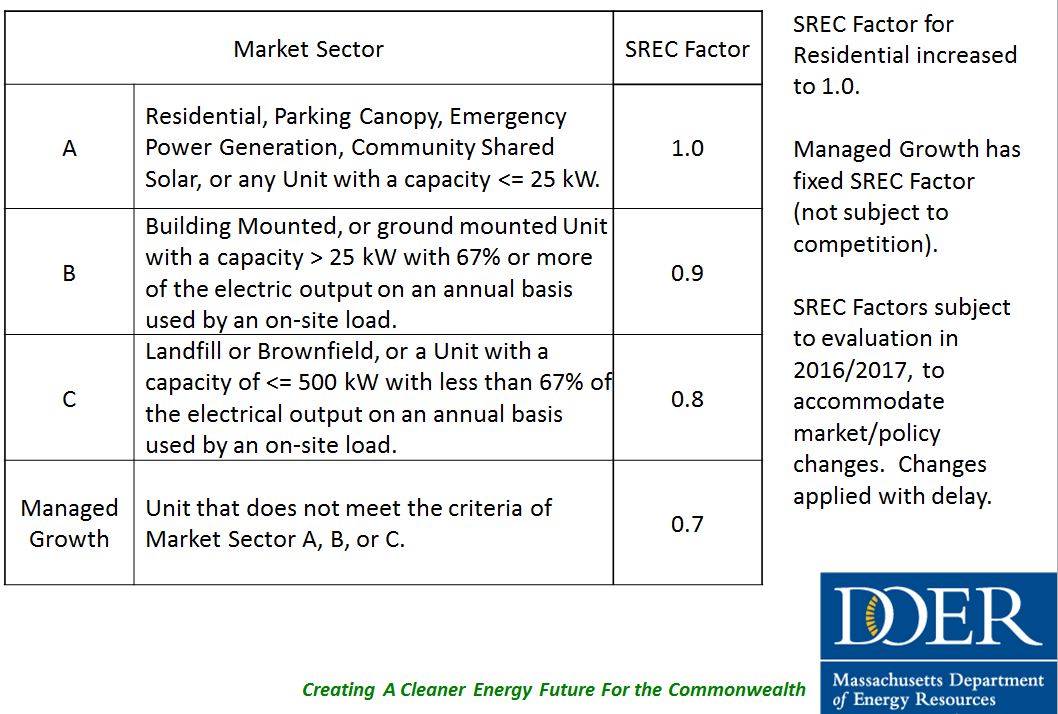

Like SREC-I facilities, SREC-II facilities will be issued 40 quarters of SREC-eligibility, based on the SREC factor times the number of MWh generated. The SREC factor assigned to a Unit in its Statement of Qualification (SQA) shall remain its SREC factor for its entire 40 quarters of eligible generation of Solar Carve-Out II Renewable Generation Attributes. Furthermore, the DOER shall complete a review of the SREC Factor Guideline no later than March 31, 2016 to take into consideration market data and analysis as well as external changes in state and federal policies and global markets. Any changes made by these guidelines shall apply to Sectors A-C for units qualified on or after January 1, 2017 and will apply to projects seeking capacity for the Managed Growth Sector in 2018. 14.05(l)4, 5.

Any excess of the SREC factor accumulated during the 40 quarters will be retired by NEPOOL-GIS. After 40 quarters of SREC-II eligibility, the system will cease to produce SREC-IIs and will begin producing Class-I credits for 100% of the MWh that the system generates. 14.05(9)(k).

Any solar photovoltaic facility larger than six MW in capacity installed on the same parcel of land and meeting all other requirements under SREC-II may qualify only for RPS Class I Renewable Generation Attributes. 14.05(9)(a). The SREC-II program capacity cap is the aggregate eligible capacity, in MW, of Solar-Carve Out II Renewable Generation Units qualified by the Department equal to 1600 MW minus the Solar Carve-Out Program Capacity Cap. 14.02.

B. Eligibility for SREC-II in the Managed Growth Sector

SREC-II facilities in the Managed Growth Sector will be eligible for qualification subject to several provisions, including annual capacity blocks, which will be announced no later than June 30 of each subsequent Compliance Year for the Compliance Year two years in the future.

- For Compliance Year 2014, the annual capacity block shall be 26 MW;

- For Compliance Year 2015, the annual capacity block shall be 80 MW. 14.05(m).

C. Procedure for Applying for an Assurance of Qualification & Financing Opportunities

The DOER will issue a full guideline outlining the process for providing Assurance of Qualification, though the draft revisions did not specify where or when these guidelines will be available. However, the revisions do specify that the content of these guidelines will be subject to stakeholder review and comment.

Section 14.05(o) details that the DOER shall grant an Assurance of Qualification for SREC-II facilities that have either:

- been granted the approval to interconnect to the grid by their local distribution company; or

- have provided evidence of the following:

(a) an executed Interconnection Service Agreement (ISA) with the distribution company; and

(b) adequate site control, interest, or other contractual right to construct the system at the location specified in the ISC; and

(c) all required governmental permits and approvals to construct the system, including building permits and notwithstanding any pending legal challenge(s) to such permits.

Section14.05(p) confirms that the DOER will establish a program utilizing ACP funds to enhance the availability of ownership financing options for SREC-II facilities. This program will be available for residential and other buildings that are owned by 501(c)(3) organizations who are incorporated under state law as not-for-profit corporations.

D. Solar Credit Clearinghouse Auction-II (SCCA-II)

Below is an overview of the Solar Credit Clearinghouse Auction under the SREC-II program. For the most part, the rules and process are similar to how the auction is run under SREC-I.

The Solar Credit Clearinghouse Auction-II for SREC-II shall be held as follows, pursuant to the draft regulations Section 14.05(9)(f)-(j):

- The first auction will be held each year on or before July 31.

SCCA-II will be available for deposits between May 16 and June 15, inclusive of these dates. A 5% fee will be assessed for all SCCA-II clearinghouse prices, pursuant to the fixed price schedule available below. All SREC-II attributes deposited into SCCA-II will be eligible for two additional years.

If the first auction clears, then the total amount of re-minted auction-II account generation attributes (SRECs) will be distributed to the bidders in a pro-rated manner based on their bid volume.

- If the first auction does not clear, then the DOER will void the auction and conduct a second auction within three business days of the first auction. The SRECs deposited into this auction will be issued eligibility for three subsequent compliance years from the year in which they were generated.

- If the second auction does not clear, then the DOER will void the auction and recalculate the Massachusetts Solar Carve-Out II Minimum Standard to adjust the demand before conducting a third auction, which will be held within three business days of the second auction. If this third auction does not clear, then the demand will be reallocated on a pro rata basis, and the excess will be returned to sellers with the previously-issued three year eligibility. These SRECs will be ineligible for future auctions.

E. Renewable Energy Portfolio Standard & Compliance Obligation Formula

The compliance obligation formulas remains the same as under 14.07(2)(d): For each subsequent Compliance Year (CY), the total compliance obligation shall be equal to the total compliance obligation from the previous Compliance Year (CY-1), plus the difference between the Solar Carve-Out Renewable Generation Attributes projected to be generated for the previous Compliance Year and the Solar Carve-Out Renewable Generation Attributes actually generated for the Compliance Year two years prior (CY-2) which is multiplied by 1.3, plus the number of Solar Carve-Out Renewable Generation Attributes from the Compliance Year two years prior banked as provided under 225 CMR 14.08(2), plus the number of Solar Carve-Out Renewable Generation Attributes from the Compliance Year two years prior deposited into the Solar Credit Clearinghouse Auction Account.

Total Compliance ObligationCY = Total Compliance ObligationCY-1 + [Total SRECs Generated (projected)CY-1 – SRECs Generated (actual)CY-2] x 1.3 + Banked VolumeCY-2 + Auction VolumeCY-2

The SREC-II Minimum Standard will not apply to the portion of load-serving entities’ (LSEs) energy sales that were subject to electricity contracts signed prior to the implementation of the program, provided that the LSE in the party to the contract provides the DOER with evidence of such contract. 14.07(3)(b).

Section 14.07(3) establishes the SREC-II Minimum Standard, which will be calculated and announced by the DOER not later than August 30 of the preceding Compliance Year as specified in the Section. 2014 and 2015 demand has already been established:

- For Compliance Year 2014, the total compliance obligation is 41,279 MWh of SREC-II generation by 85 MW of SREC-II capacity across the sectors. 14.07(3)(c).

- The total compliance obligation for Compliance Year 2015 is 161,958 MWh, generated by 230 MW of SREC-II capacity across the sectors. 14.07(3)(d).

For each subsequent Compliance Year (CY), the total compliance obligation shall be determined by the DOER as equal to the sum of the following quantities of generated and projected SREC-IIs:

- Installed SREC-II Supply (installed facilities);

- Qualified but not Installed SREC-II Supply (facilities that have been initiated but are not yet online);

- Projected New Supply (based on prior growth trends by market sectors and annual capacity blocks, such that cumulative installed capacity does not exceed the cumulative installed capacity target for the end of the year as follows);

- Rollover Volume (those SREC-IIs that remain eligible for compliance from re-minted SCCA-II generation and banked SREC-IIs); and

- Third Round Auction Volume Doubling (in the case of a third round SCCA-II).

Section 14.07(3)(g) assures that the DOER will provide a clear and precise methodology by which it will calculate the quantities set forth above and the Compliance Obligation.

After 2020, the RPS Class I Minimum Standard shall increase by 1% per Compliance Year unless modified by law. 14.07(4).

As the rulemaking process continues, we will provide updates and additional analysis on this blog.

Tweet