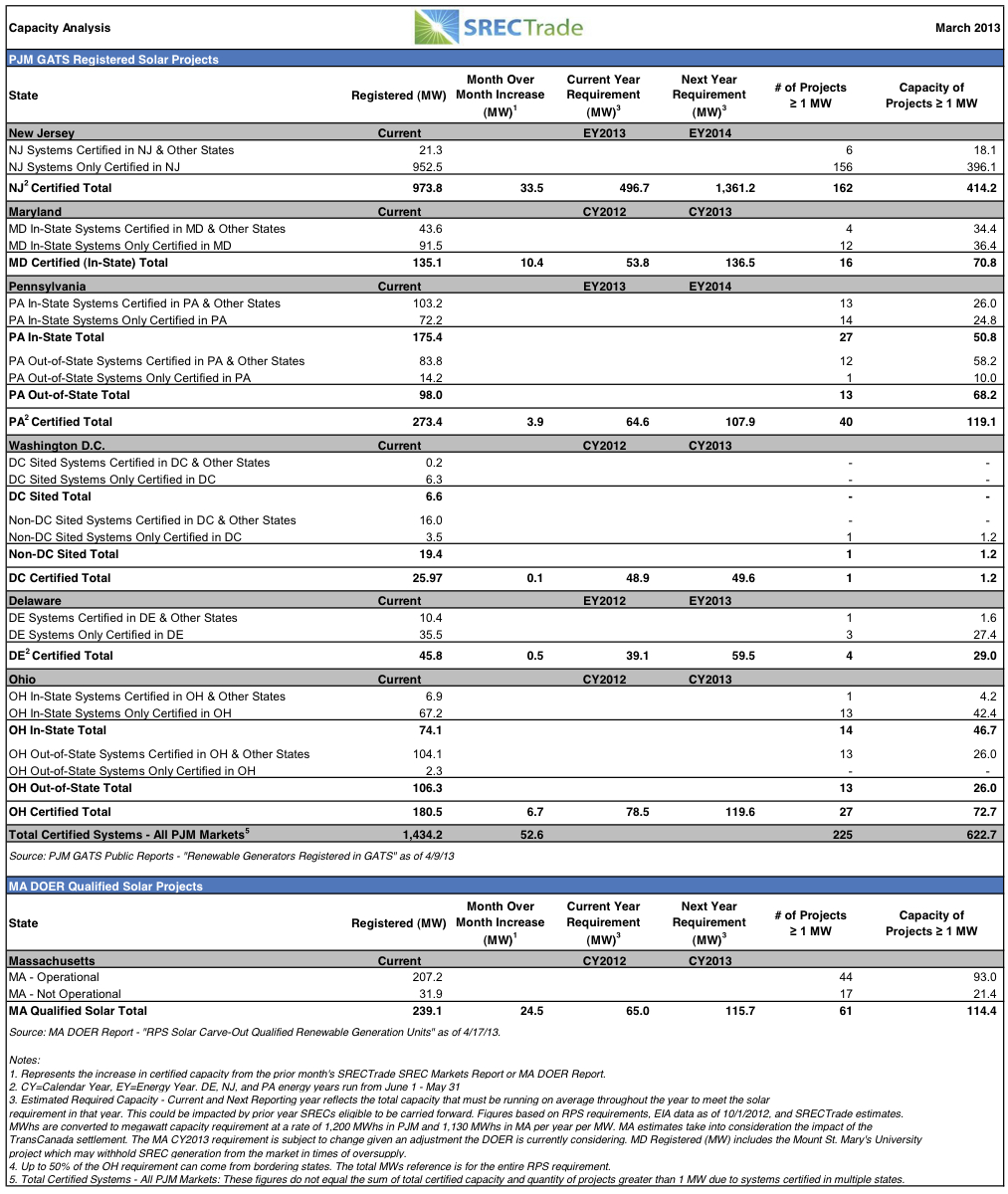

SRECTrade’s June 2013 SREC Auction closed on 6/04/13. Below are the clearing prices by vintage across the markets covered in the auction.

| June SREC Prices | SREC Vintage Year | ||

| State | 2011 | 2012 | 2013* |

| Delaware | – | $35.00 | – |

| Maryland | $107.00 |

$115.00 | $122.50 |

| Massachusetts | – | $215.00 | – |

| New Jersey | $115.00 | $125.00 | $130.00 |

| Ohio In-State | – | – | – |

| Ohio Out-of-State | $14.00 | $14.00 | $14.00 |

| Pennsylvania | – | $10.00 | $11.00 |

| Washington, DC | – | – | $488.98 |

Notes:

*Delaware, New Jersey and Pennsylvania operate on a June-May energy year. For example, current vintage SRECs are generated beginning in June of 2012.

Green text represents a price increase over the last auction clearing price for that vintage, red text represents a decrease. “-” reflects no sale, which would result if there were no SRECs available for sale in that vintage or there were no matching bids and offers to determine a clearing price.

State Market Observations:

Delaware: Current vintage DE SRECs traded at $35/SREC. The primary buyer for DE SRECs is Delmarva Power and Light (DPL). Most SRECs are sold through DPL’s SRECDelaware program, for which SREC asset owners submit competitive applications in order to obtain 20 year SREC contracts. There continues to be some need for SRECs outside of DPL’s program and compliance buyers with a need for DE sited but non-DPL derived demand will decline over time. SRECTrade administers both the DPL spot auction as well as the software behind the the SRECDelaware solicitations.

Maryland: MD eligible SREC prices came down again from last month’s SRECTrade auction prices. MD2011s, MD2012s, and MD2013s transacted at $107.00/SREC, $115.00/SREC, and $122.50/SREC, respectively, in the June auction.

Massachusetts: The MA2012 auction price increased from $200/SREC in May to $215/SREC in the June auction. Unsold SRECs need to be deposited in the DOER Solar Credit Clearinghouse Auction NEPOOL-GIS account by June 15, 2013. SRECs that are not deposited in the DOER auction will not be eligible for future transactions. SRECTrade expects that approximately 45,000 SRECs will be deposited in the DOER auction. For the latest info on the MA market read our MA blog posts.

New Jersey: NJ SREC prices declined in the June auction. NJ2011, NJ2012, and NJ2013 SRECs traded at $115.00, $125.00, and $130.00/SREC, respectively. The New Jersey market remains over-supplied. Excluding unsold SREC supply carried over from previous vintages, approximately 496.7 MW of annual installed operational capacity is required to meet the 2013 requirement. As of, 5/31/2013, the NJ Office of Clean Energy reported that 1,078.4 MW had been installed in NJ.

Ohio: No transaction occurred for OH sited SRECs this auction period. OH2011, 2012 and 2013 adjacent vintage SRECs traded at $14/SREC. 2013 is expected to continue to experience oversupply and minimal demand. Most demand for OH Sited SRECs has been fulfilled through long term agreements with large utility scale projects or through long term RFPs with the state’s regulated utilities.

Pennsylvania: PA2012 and 2013 SRECs traded at $10/SREC respectively, in line with previous auctions. SREC oversupply will continue to lead depressed SREC pricing for the foreseeable future.

Washington, DC: DC SRECs continue to increase in value. DC 2013 vintage SRECs traded at $488.98. It is expected the market will continue to experience under supply into the 2013 trading year.

For historical auction pricing please see this link. The next SRECTrade auction closes on Tuesday, July 2nd at 5 p.m. ET and will cover PJM SRECs only. Click here to sign in and place an order.

Any unsold MA 2012 SRECs should be deposited in the the DOER auction NEPOOL-GIS account by June 15th. SRECTrade will automatically transfer unsold MA SRECs for its EasyREC clients. This June 15th deadline only affects facilities that are sited in MA and eligible for the MA SREC program.

Tweet